|

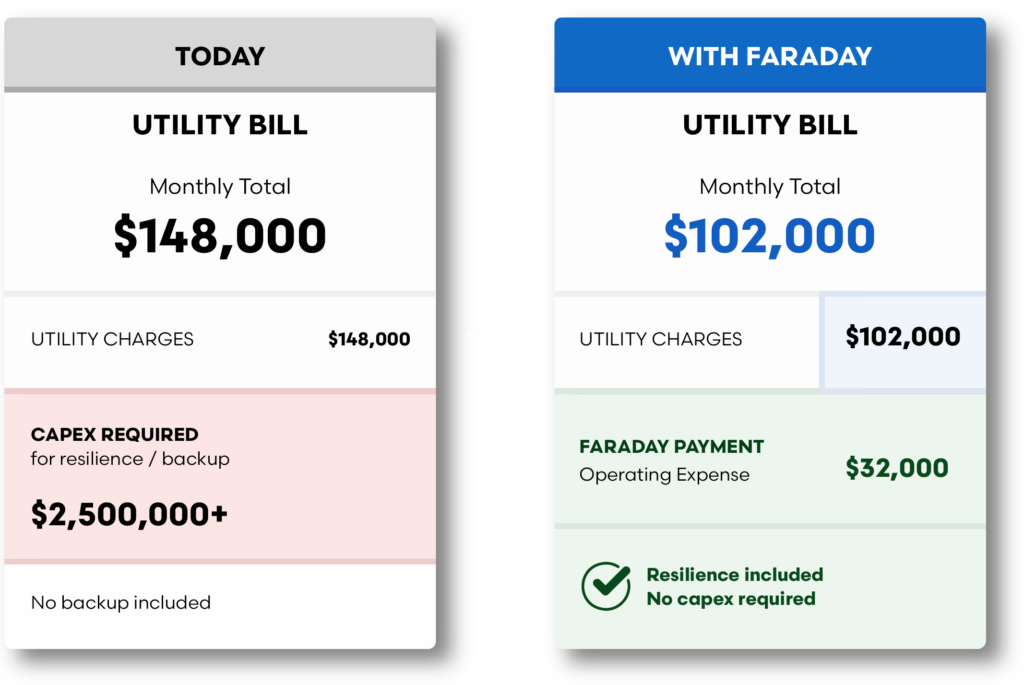

STATUS QUO

(YOUR BILL TODAY) |

WITH FARADAY + PPA

|

|---|---|

|

Utility bill: full amount, monthly

|

Utility bill: lower (you keep paying the utility, but for less energy)

|

|

Capex required: separate, for any backup or resilience investment

|

Faraday payment: operating expense, monthly.

|

|

Demand-charge exposure: full

|

Demand-charge exposure: reduced.

|

|

Outage exposure: full

|

Outage exposure: 4–12 hours of selected critical loads covered

|

|

Energy cost trajectory: rising at 4–7% per year

|

Energy cost trajectory: rising at 4–7% per year

|

|

Net effect: —

|

Net effect: a piece of your utility bill replaced with a more predictable monthly expense

|

|

Attribute

|

FARADAY PPA

|

EQUIPMENT LEASE

|

CASH PURCHASE

|

|---|---|---|---|

|

Capex required from host

|

$0

|

$0 (FMV operating lease) to ~10–20% (capital lease, varies)

|

Full project cost

|

|

Monthly cost structure

|

$/kWh × actual generation, or fixed $/month

|

Fixed monthly lease payment

|

Capital outlay year 1; no monthly payment after

|

|

Counterparty

|

Faraday (PPA financier)

|

Equipment lessor (tax-equity or bank partner)

|

Host owns equipment

|

|

Accounting treatment

|

Operating expense; off-balance-sheet for most commercial structures

|

Operating lease (ASC 842 ROU asset + liability) or capital/finance lease

|

Capex; depreciable asset on balance sheet

|

|

Tax treatment

|

ITC monetized at Faraday-side financing entity; pass-through pricing reflects monetization

|

ITC monetized by lessor; pass-through pricing reflects monetization

|

Host claims ITC directly (if tax appetite exists); MACRS depreciation

|

|

Term length

|

Typically 15–25 years

|

Typically 10–15 years

|

Ownership in perpetuity

|

|

End-of-term options

|

Renew, buy out (FMV), or remove

|

Renew, buy out ($1 or FMV per structure), or return

|

N/A

|

|

Resilience / backup scope

|

Included in Faraday system per tier

|

Included in Faraday system per tier

|

Included in Faraday system per tier

|

|

Site relocation / acquisition

|

Assignment with Faraday consent

|

Assignment with lessor consent

|

Asset moves with sale or relocation

|

|

Best fit for

|

Buyers prioritizing zero capex, off-balance-sheet treatment, no tax appetite

|

Buyers wanting operating-lease treatment, balance-sheet flexibility, eventual ownership

|

Buyers with ITC monetization capacity, asset-ownership strategy, internal IRR target

|

|

OUTCOME (YEAR 1)

|

FARADAY PPA

|

EQUIPMENT LEASE

|

CASH PURCHASE

|

|---|---|---|---|

|

Capex from host

|

$0

|

$0

|

$20,000,000

|

|

First-year P&L impact

|

Operating Expense

|

Lease Expense

|

Depreciation + Interest

|

|

Who own/reg. savings (est.)

|

$1,150,000

|

$1,050,000

|

$1,300,000 - $1,500,000

|

|

10-year net savings (est.)

|

$11.5M+

|

$10.5M+

|

$13M - $1M+

|

|

Balance sheet impact

|

Off balance sheet

|

ASC 842 (ROU asset + liability)

|

Asset on balance sheet

|

|

End of term

|

Renew / Buy out (FMV) / Remove

|

Renew / Buy out ($1 FMV) / Return

|

Own in perpetuity

|

PPA Structure

Faraday-provided PPA financing. You sign the PPA with Faraday; Faraday holds the customer relationship and is the counterparty for the energy agreement. One contract, one counterparty, across the life of the system.

Equipment Lease Structure

Faraday works with equipment leasing companies (tax equity or specialty finance companies). Equipment lease company owns the project but leases to Faraday to manage EPC and O&M services. Selected for tax advantages or future ownership.

Cash Purchase Structure

No financing counterparty. The host facility funds and owns the equipment. Faraday delivers under direct EPC and O&M contracts with the host.